The world of Connected TV (CTV) is about to reach boiling point. Netflix and Disney+ are included in a group of high-profile entrants to the ad-supported market in 2022, as streaming businesses combat rising levels of subscriber churn with ad-funded subscription tiers.

At our Full Stream Ahead for Ad-Supported CTV in 2023, a hybrid event hosted at Total Media’s offices in Soho and (appropriately) live-streamed to viewers at home through LinkedIn, a group of industry experts gathered for a panel debate moderated by Propeller Group’s Executive Chairman Martin Loat. IThe panel included:

• Alex Hole, Vice President & GM, Samsung Ads Europe

• Katie Coteman, Vice President Advertising & Partnerships, Warner Bros. Discovery

• Patrick Kelly, Head of Digital, ITV

• Gill Hind, Chief Operating Officer, Enders Analysis

• David Cottell, Programmatic Senior Lead, Channel Four

The session explored how CTV is changing advertising, and what recent initiatives mean for media planners and buyers, brand-side marketers, the wider advertising technology ecosystem and millions of consumers at home. And as this is a acronym-heavy business, here’s a glossary to help readers keep pace:

• CTV = Connected TV; is a device that connects to—or is embedded in—a television to support video content streaming. Brands providing ways to access CTV include Samsung, Xbox, PlayStation, Roku, Amazon Fire TV, Apple TV, and more.

• VOD = Video on demand; any video service that offers videos, TV or movies available at a viewer’s convenience. With VOD, viewers can choose what to watch, when they want. Popular examples of Video on Demand businesses include Samsung TV Plus, Netflix, Disney+, Hulu and many more online streaming services

• OTT = Over the top; streaming video content distributed directly through the internet – bypassing traditional distribution. Examples include HBO Now, Hulu, Netflix, Amazon Video, YouTube/YouTube Red.

• AVOD = Advertising-based video on demand; free streaming services funded by advertising - the most used international AVOD service in the UK is Pluto TV, followed by The Roku Channel.

• SVOD = Subscription video on demand; the most well-known examples of SVOD services are Disney+, Netflix or Amazon’s Prime Video.

• BVOD = Broadcaster video on demand; BVOD platforms let users stream content developed by established TV broadcasters and examples include BBC iPlayer, ITVX and Channel 4.

• FAST = Free ad-supported streaming television; FAST offers linear channels that are supported by advertisements. In other words, FAST operates like traditional linear TV but is delivered through streaming platforms. Examples include Samsung TV Plus.

• CPM = Cost per mille; cost per thousand impressions for advertisers

Before the panel began, Gill Hind of Enders Analysis shared some insights into how the CTV space was growing – and what it means for broadcasters, advertisers and audiences – in an exclusive report for our audience.

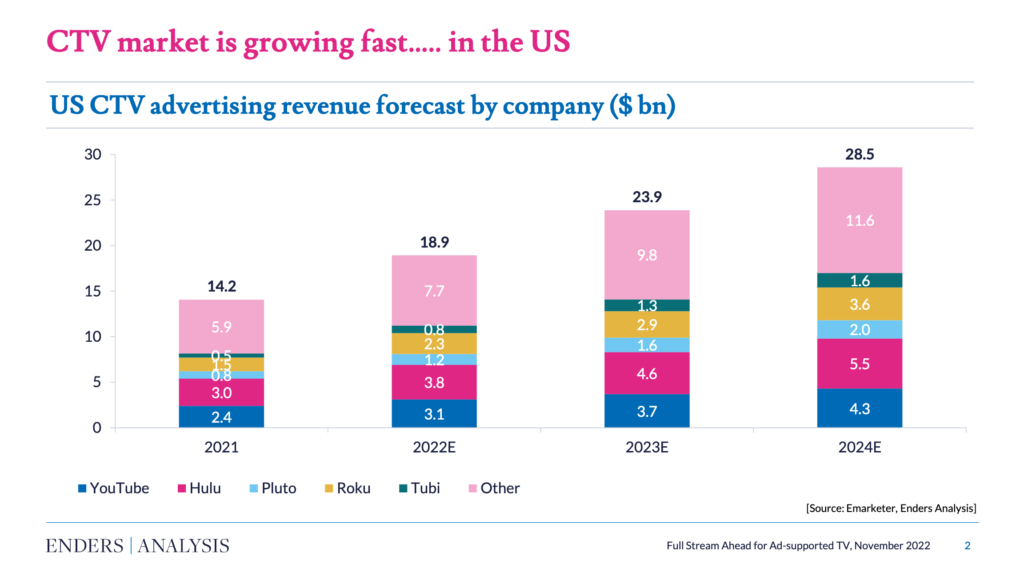

CTV market is growing FAST

The CTV market is growing fast in the US. “It’s up 33% this year,” Gill noted. “Which is significantly more than linear which is only up 8%.”

FAST services are driving much of the growth. These services have generally included both ad-supported on-demand video libraries (or AVOD), alongside online linear channels (FAST channels).

Gill pointed out that they typically focus on specific genres or shows – such as the Baywatch channel. And they appeal to broadcasters as they are cheap to run, leverage third-party programming that has little value elsewhere and tap into familiar broadcast-style ‘lean back’ need states.

The growth is slower in Europe, she added. “Unlike the US, the UK is already well catered for in free video—with the public service broadcasters investing heavily in the space and continuing to provide high quality content.”

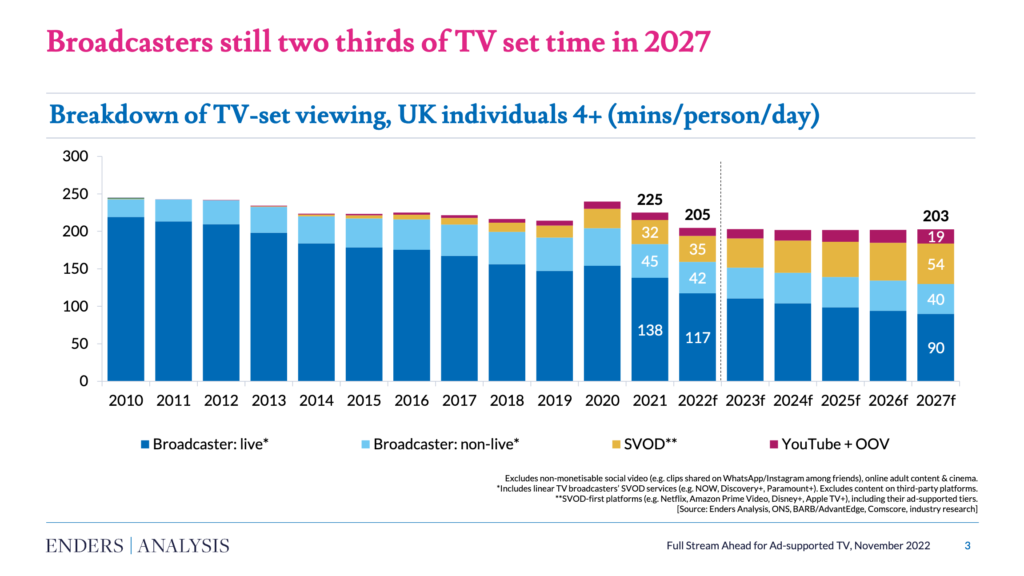

Broadcast still on top

Gill pointed to a chart detailing audience viewing habits that showed live and recorded broadcasts still make the bulk of viewing time, although they lost significant share to SVOD over the last five years. “In the next five years, SVOD first platforms such as Netflix will make up about a quarter of TV set viewing, while YouTube and ‘Other Online Video’ (such as TikTok) will be about 10%.”

“Our view is that over the next five years, while FAST may make some inroads into the market, revenue will be very small compared to the BVOD market.”

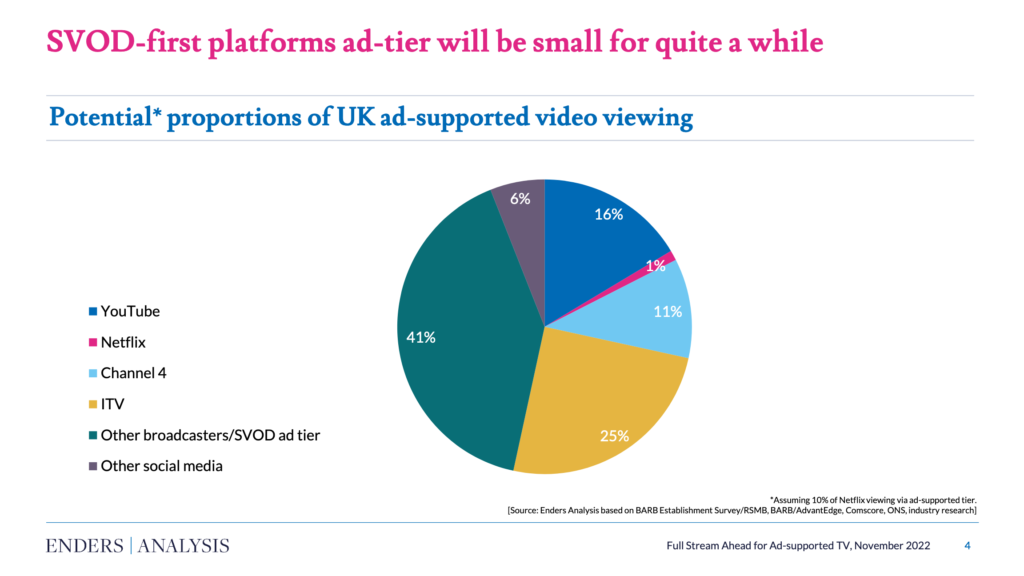

SVOD-first ad tier isn’t going to make a big splash

Though Netflix’s entrance into the advertising market has sparked excitement, Gill Hind noted they needed to overcome some significant hurdles.

“Netflix has conditioned people to see advertising as annoying. And now the service on offer is lower quality, with less content and unskippable ads. The uptake isn’t likely to be huge.”

“But I think it’s great for the markets,” Gill summarised. “There will be more high-quality inventory within the UK marketplace – especially when targeting younger demographics where TV ad price inflation is most severe due to declining linear viewing.”

“However, they also want to understand the incremental reach and frequency that Netflix can deliver above and beyond their TV/BVOD campaigns. This is also true for AVOD. Measurement across all video viewing becomes key.”

(How) are you still watching?

The panel kicked off by debating Gill’s final remarks and the implications of Netflix’s foray into advertising.

Alex Hole of Samsung Ads agreed that “It will be interesting to see how much this changes in a year. Our data at Samsung shows that the number of devices used exclusively for streaming has risen from 19% to 23% in the last two years. Almost 50% of TV viewers now watch less than three hours of linear TV per month. This is a challenge for advertisers and one which makes the Netflix offer interesting – but I don’t believe that it will impact linear TV budgets in the near term.”

But Alex challenged the notion that FAST services aren’t growing in Europe.

“Our data paints a slightly different picture. Samsung TV Plus has over 1000 channels across Europe and we are experiencing monthly growth. But CTV is filled with acronyms and anonymous measurements – it is our job to educate the buying community who lean towards VOD and linear instinctively.”

David Cottell of Channel 4 added context to an on-screen graph from Gill’s presentation which illustrated the rise of SVOD viewing and steady decline of linear. “It’s important to take into account that opportunities for monetisation have emerged alongside this”, he continued.

“In 2010, a huge amount of TV viewing was still done via recordings. Now we have VOD which is much easier to monetise against and more useful for advertisers. All4 [now rebranded] got 1.5 billion views in 2021 – which is 3x as many as it did in 2015.”

Netflix’s challenges

Katie Coteman of Warner Bros. Discovery picked up on this point. “In the traditional pay TV environment, we have always needed multiple revenue streams. Content is expensive. You need revenue from both subscriptions and advertising.”

“But Netflix’s biggest challenge is delivering the ads effectively,” she continued. “It can’t be a frustrating or poor experience. Advertising has to be intelligently placed, personalised and not clash with content – or the value exchange for viewers will quickly fall out of line. It needs short ad-breaks which are high quality – efficient targeting and good environments.”

She pointed out that most Netflix Originals are created without ad breaks in mind – which means Netflix has to exclusively use pre-roll ads. And it doesn’t have the rights to put advertising next to some of its partner content.

“All of this adds up to a fairly complex offer. Netflix needs to simplify things for buyers and advertisers who generally just want to extend the reach of their media campaigns.”

Patrick Kelly of ITV argued that it was more of a reactive move, as opposed to a strategic one. “Netflix is a great service with great content. But this feels like a response to share-price. At ITV, we spend over £1bn on TV to monetise our content. It’ll be a huge challenge for Netflix’s new tier to offset content expenditure. Scott Galloway in the US said that $3000 is spent per household on content – and I don’t think that a £2 discount on subscriptions will cover that gap.”

Measurement matters

The panel agreed that the success of any advertising-funded SVOD service is dependent on the metrics it can provide marketers.

David pointed to Netflix’s rumoured CPM of £50, which is perceived as expensive.

“I would like to say I am, naturally, a massive supporter of agencies paying £50 CPM for premium long form video content! To be fair to Netflix, it should be expensive. The range in quality in the Video ad market from one publisher to the next is massive, so it’s right that they put a premium on their inventory”.

“Once the excitement at being able to place campaigns on Netflix expires – the streaming service will need to upgrade its measurement and targeting massively to justify that CPM.”

Patrick picked up on this. “Price is largely irrelevant. If you can prove it is effective, advertisers will pay for it. But demonstrating effectiveness is difficult in CTV – there are no cookies and there is no BARB. If you want ad-spend, you need to be able to show how you drive incrementality – growth that can be directly attributed to specific marketing efforts above and beyond the existing brand equity”.

“Overall consumption of TV isn’t changing – audiences are just moving through new services,” summarised Alex. “CTV enables advertisers to do much more sophisticated targeting as viewership fragments. And that’s why we need independent attribution and measurement to help advertisers establish effectiveness.”

To catch the full discussion, watch the VOD of the panel below or on Propeller’s YouTube channel. And see the full breakdown of the streaming market in the Enders Analysis report here. If you have any questions, or wish to learn more about Propeller Group and our services, get in touch with: Ben.Titchmarsh@propellergroup.com